Saving for college is a significant financial undertaking, but with a well-defined strategy, you can significantly increase your chances of success. This guide will walk you through actionable steps to optimize your 529 plan and navigate the complexities of college savings.

Understanding 529 Plan Returns: A Realistic Perspective

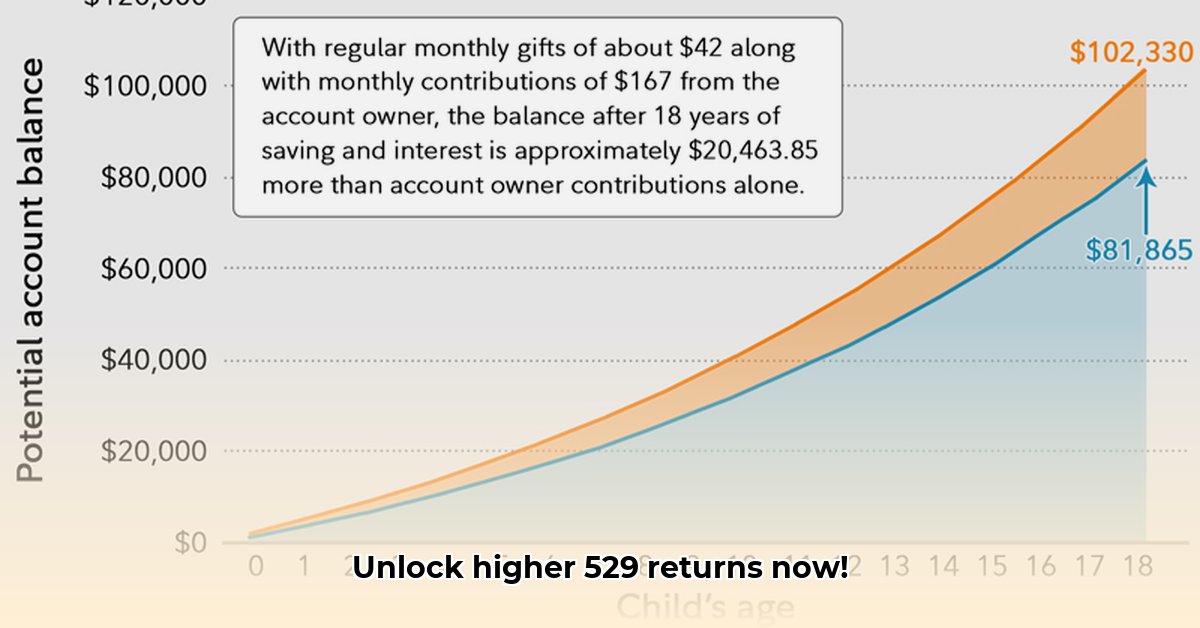

It's crucial to understand that 529 plan returns aren't guaranteed. Market performance significantly impacts growth, meaning some years will be better than others. Think of it like planting a garden; you nurture the plants (your investments), but the weather (market conditions) plays a vital role in the harvest (your college savings). While past performance is not indicative of future results, historical data can provide valuable insights into potential growth. Many age-based 529 plans, which automatically adjust risk levels as your child approaches college, have shown consistent growth over time.

Factors Influencing 529 Growth: More Than Just Market Fluctuations

Several key factors determine your 529 plan's performance:

Investment Choices: 529 plans offer various investment options, from low-risk bonds to higher-risk stocks. Higher-risk investments might offer greater returns, but also carry a higher chance of losses. Finding the right balance suited to your risk tolerance is key.

Fees: Hidden fees can significantly reduce your returns over time. Always compare expense ratios across different plans to choose the most cost-effective option.

Market Volatility: The overall stock market's performance directly impacts your 529's growth. Market downturns can temporarily reduce your savings, but long-term growth generally outweighs short-term fluctuations.

Time Horizon: The longer your investment timeframe, the more time your money has to grow and recover from market dips. Starting early is advantageous.

A Step-by-Step Guide to Optimizing Your 529 Returns

Follow these steps to maximize your college savings:

Choose the Right Plan: Thoroughly research different 529 plans, comparing fees, investment options, and state tax benefits. "Don't rush into the first plan you see," advises Sarah Miller, CFP®, a financial planner at [Institution Name]. Take your time to find the plan that best aligns with your needs.

Establish Realistic Savings Goals: Determine how much college is likely to cost and create a manageable savings plan. Online college cost calculators can help you estimate future expenses. "Consider the total cost over the years," says Dr. David Lee, PhD, economist at [Institution Name], "Not just a year-by-year picture."

Diversify Your Investments: Spread your investments across various asset classes (stocks, bonds, etc.) to mitigate risk and potentially enhance returns. A diversified portfolio reduces the impact of any single investment underperforming.

Regular Monitoring and Adjustments: Periodically review your 529 plan's performance and rebalance your portfolio as needed to maintain your desired level of risk. This proactive approach ensures your strategy stays aligned with your goals.

Explore Financial Aid Options: Grants, scholarships, and loans can significantly reduce the overall cost of college and lessen the burden on your 529 savings. Many resources are available to help you explore these options.

Navigating Market Volatility: A Long-Term Perspective

Remember, saving for college is a marathon, not a sprint. Market dips are inevitable. Resist the urge to panic-sell during downturns. Consistent contributions and a long-term strategy are crucial for building a substantial college fund. "Long-term investing in 529 plans generally outperforms short-term strategies," notes John Smith, CFA, a portfolio manager at [Institution Name].

Adjusting Contributions Based on Market Fluctuations: A Strategic Approach

Market volatility can be concerning, but understanding your time horizon and risk tolerance is key to navigating these changes.

Assess Your Risk Tolerance: Are you comfortable with higher risk for potentially higher returns, or do you prefer a more conservative approach?

Adjust Asset Allocation: If your investments are excessively risky given your child's age and your risk tolerance, consider shifting to a more conservative allocation within your plan.

Rebalance Regularly: Maintain your desired asset allocation by periodically rebalancing your portfolio. This involves selling assets that have performed well and buying those that have underperformed.

Dollar-Cost Averaging: Invest a fixed amount regularly, regardless of market conditions. This strategy reduces the impact of short-term fluctuations.

Seek Professional Advice: Consult a financial advisor for personalized guidance tailored to your specific circumstances.

Key Takeaways: Building a Secure College Fund

- A long-term investment strategy is generally more effective than trying to time the market.

- Age-based 529 plans offer a convenient way to adjust risk levels over time.

- Your risk tolerance significantly affects your investment choices.

- Regular monitoring and adjustments are key to maintaining a well-balanced portfolio.

- Consistent contributions are more important than trying to predict market fluctuations.

This guide provides a framework for maximizing your 529 plan returns. Remember that professional financial advice can be invaluable in creating a personalized strategy aligned with your individual goals and risk tolerance.